How To Offer Finance For Restaurant Equipment

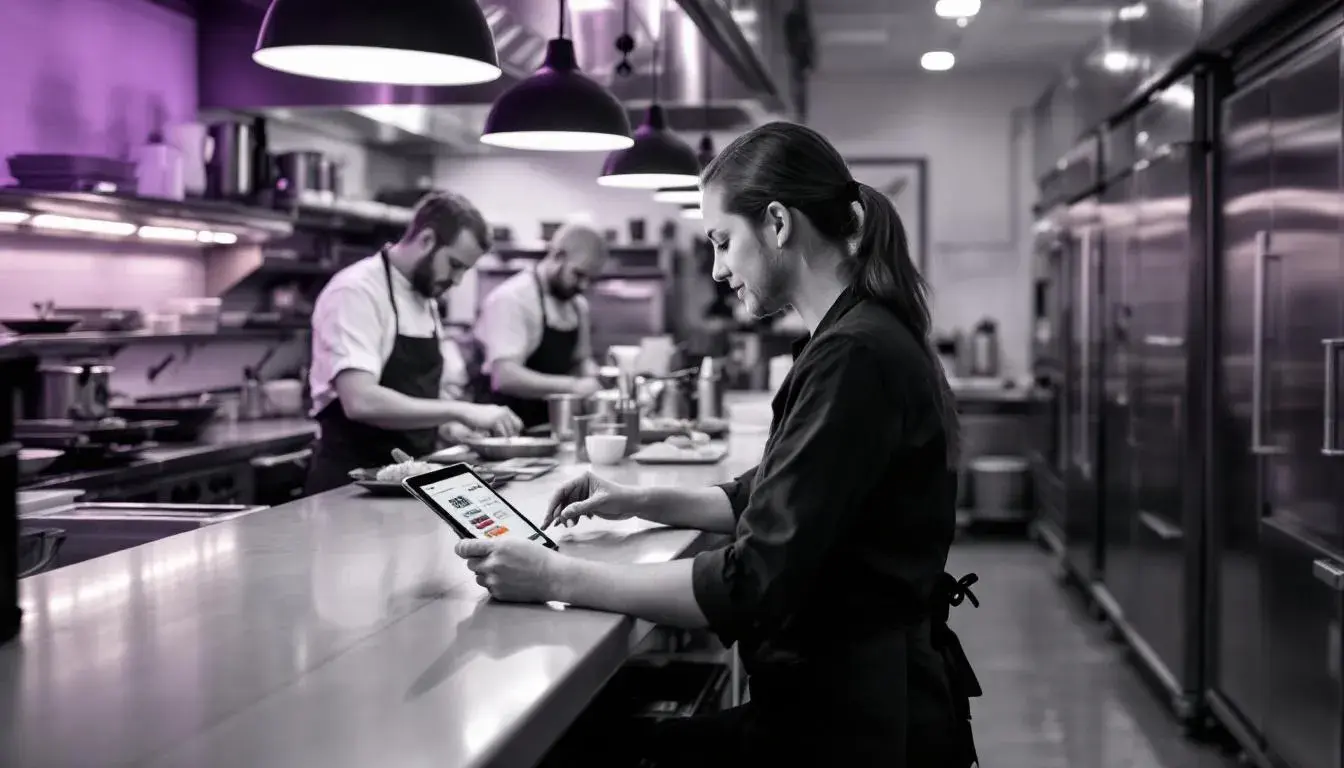

Banner image concept

A modern, bright commercial kitchen in a UK restaurant. Chefs prep food using high-spec financed kit such as an industrial oven and refrigeration. A tablet displays a simple finance calculator or lease agreement, signalling fast, accessible funding.

What customer finance really is in practice

Customer finance lets your buyers spread the cost of restaurant equipment across fixed monthly repayments, rather than paying in full on day one. For your business, it is a sales tool that removes budget friction while keeping your invoice value intact. Done well, it supports bigger baskets, faster decisions and more predictable conversion, especially when customers are comparing suppliers on more than just headline price. In the UK, equipment finance is typically structured as a lease or fixed-term credit agreement, with applications designed to be quick and decisioning driven by the customer’s circumstances and the asset being funded.

Why restaurant buyers lean on finance

Restaurant operators often have cash tied up in stock, wages, rent and fit-out costs, so even profitable businesses can prefer to preserve working capital. Newer ventures and expanding sites may also want to keep contingency funds available for unexpected costs during opening weeks. In catering equipment specifically, specialist leasing providers commonly report very high acceptance rates, including for new businesses, which makes finance feel like a realistic option rather than a last resort. Many operators also like the simplicity of predictable monthly payments and the ability to upgrade equipment as menus, volumes and energy-efficiency needs change.

How offering finance can lift conversion and order value

When you present finance alongside the cash price, you change the decision from “Can we afford this?” to “Does this payment fit our cash flow?” That shift is powerful in a sector where timing matters and downtime is expensive. Finance can also reduce discount pressure because customers focus less on a single large outlay. It supports higher-spec choices (for example, moving from entry-level to energy-efficient refrigeration) and can speed approvals for refurbishments and replacements. In practice, vendors that offer low minimum ticket options can finance everything from a single POS terminal to a full kitchen package, giving you more opportunities to win the sale at the moment the customer is ready.

Typical transaction values you may see

| Deal size band | Common use cases | Typical finance fit | Notes for suppliers |

|---|---|---|---|

| £500 to £2,500 | Small appliances, POS, replacement items | Shorter terms, low minimum programmes | Useful for removing friction on add-ons and spares |

| £2,500 to £15,000 | Single major item, refrigeration, extraction components | Lease-to-own or fixed-term credit | Often the sweet spot for independents |

| £15,000 to £75,000 | Partial kitchen refit, multiple assets | Structured lease with fixed monthly payments | Strong opportunity to increase average order value |

| £75,000 to £250,000 | Full kitchen build, multi-site rollouts | Asset finance with tailored terms | Documentation and financials matter more |

| £250,000 to £500,000 | Large fit-outs, production kitchens | Specialist lender matching | Longer underwriting, but achievable with the right package |

Restaurant equipment customers commonly finance

Commercial ovens, combi ovens and ranges

Refrigeration and cold rooms

Dishwashers and glasswashers

Ventilation and extraction systems

Preparation equipment (mixers, slicers, processors)

Coffee machines and bar equipment

POS, kiosks and kitchen display systems

Energy-efficient upgrades and replacement programmes

FCA and compliance: what you must get right

Offering finance means communicating clearly and fairly, keeping promotions balanced and avoiding any pressure selling. You should not present finance as guaranteed, and you must be careful with any statements about costs, approvals or savings. If you are introducing customers to a broker or lender, your role, permissions and responsibilities need to be clear, including how customer data is used and what the customer is applying for. Ensure your website and sales scripts align with FCA expectations, and keep records of the journey.

How introducer and broker models typically operate

Most equipment suppliers do not want to become a lender. Instead, they act as an introducer and partner with a broker who can source suitable lending options across multiple funders. You focus on the sale, the customer selects a finance option, and the broker manages the application and lender matching. This model can be particularly effective in catering equipment because lenders often treat the asset as part of the security and can offer structured products such as Fair Market Value leases, lease-to-own agreements, or £1 buyout options. It also helps you serve a wider spread of customers, from start-ups to established groups, without forcing a single lender’s criteria onto every deal.

Understanding APR isn’t just about percentages - it’s about knowing what you’ll pay in real terms.

The customer journey, step by step

Show finance early: Display “from £X per month” alongside the cash price on product pages, quotes and proposals.

Confirm eligibility basics: Check the customer is a UK business, understands it is business finance, and has the right decision-maker involved.

Collect a light application: Business details, owners/directors where required, equipment list, supplier quote and delivery timeline.

Run a finance search: Broker matches the deal to suitable lenders based on ticket size, asset type and customer profile.

Receive a decision: Often quickly for straightforward deals; more complex fit-outs may need financials and projections.

Select structure and term: Choose between options such as FMV, lease-to-own or £1 buyout, and align term length to cash flow.

Sign documents: E-signature where possible to keep momentum.

Supply and install: Equipment is delivered, installed and verified per lender requirements.

Payout and servicing: Supplier is paid (typically once conditions are met) and the customer repays monthly.

Standout: what to offer on every quote

A clear cash price

A monthly price example with term length

A simple note on what affects approvals (business profile, affordability, documentation)

Getting started with Kandoo

Kandoo helps UK businesses offer finance in a way that supports conversion without adding operational headaches. We work with you to shape a finance offer that fits your typical basket size, customer profile and sales process, whether you sell online, in a showroom or via field sales. The aim is simple: make finance feel like a normal part of buying equipment, not a separate conversation. Once live, you can build finance into quotes and marketing, and we will support you with the onboarding steps, journey design and ongoing optimisation so you can focus on selling.

Next steps you can take this week

Add a finance prompt to your top 10 best-selling products

Train your team to present monthly costs alongside cash prices

Prepare a simple checklist of documents for larger deals (latest accounts, bank statements where needed, equipment schedule)

FAQs

What finance products are most common for restaurant equipment?

Leasing is widely used for catering equipment because it can reduce upfront cost and keep payments predictable. Depending on the lender and deal, options can include FMV leases, lease-to-own and £1 buyout structures.

What APR should my customers expect for equipment loans?

Rates vary by lender, term and credit profile. Across the market, equipment loans are often priced within a broad range, commonly around 8% to 30% APR, with stronger profiles typically accessing lower rates.

Can new restaurants get approved for equipment finance?

Yes. Specialist catering equipment finance providers often report very high acceptance rates, including for new businesses, which can make funding achievable even with limited trading history.

Do customers need to pay a deposit?

Not always. Many equipment leasing arrangements can be set up with minimal or no upfront deposit, although this depends on the lender, the customer profile and the asset.

Is leasing tax efficient for UK businesses?

Lease payments are often treated as an operating expense, which may be tax deductible, subject to the customer’s circumstances and their accountant’s advice.

How quickly can finance be arranged?

Simple deals can be progressed quickly, sometimes within days, especially where the application is complete and the equipment list and supplier quote are clear. Bank-style lending routes can take longer.

What documents might a lender request?

For larger or higher-value deals, lenders may ask for recent financial statements, visibility of existing debt and evidence of turnover, alongside a clear equipment schedule and delivery plan.

Will offering finance affect my margins?

It can protect them. When customers evaluate affordability via monthly payments, you may face less pressure to discount. Your commercial setup depends on the finance arrangement and how you present it.

Do I need to be FCA authorised to offer finance?

It depends on your role and how you introduce finance. Many suppliers use an introducer model, partnering with a broker who manages regulated elements where applicable. You should take guidance based on your specific setup.

How do I present finance without confusing customers?

Keep it simple: show cash price and a representative monthly example with term length, explain that approvals depend on the customer’s circumstances, and offer a clear route to apply.

Buy now, pay monthly

Buy now, pay monthly